By Max Street

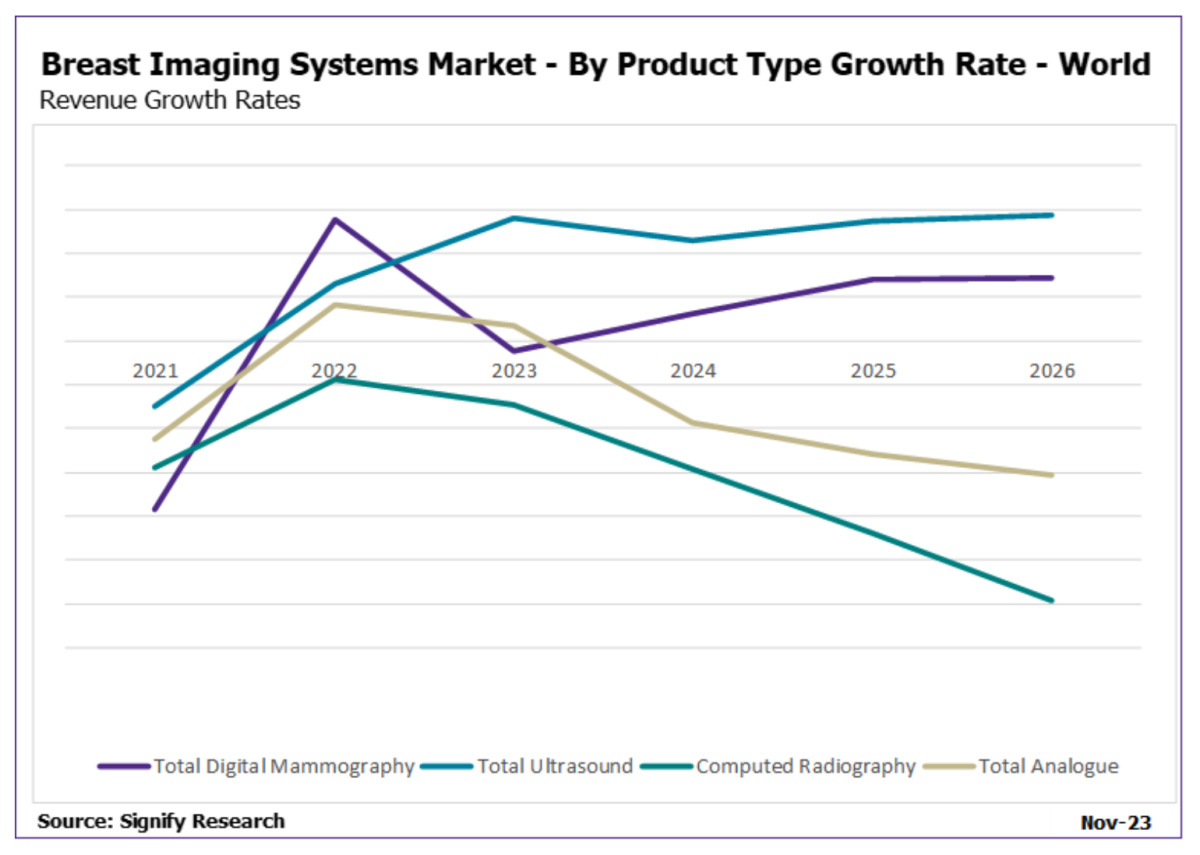

2023 stood out as a turning point for the breast imaging market, due to the diminished impact of COVID-19 and a rebalance in market demand. In 2022, breast imaging revenue was down 17.6% compared to 2021 as vendors suffered a shortage of semiconductors, inflation hikes, and a market correction following elevated investment in breast imaging systems in 2021, as budgets returned post-COVID.

Overall, breast imaging revenue grew 12.5% in 2023 and is forecast to reach $1.18 billion by 2027. This is driven by introduction of novel screening programs, digitalisation within developing countries, and an increasing proportion of digital breast tomosynthesis (DBT) and automated breast ultrasound (ABUS) system purchases.

Ad Statistics

Times Displayed: 10528

Times Visited: 32 Brand-New FDA-cleared Advanced Ultrasound Medical Device available for sale or lease to Wound Care Centers or any other Medical Facilities.The Arobella 1000D is designed for non-contact or debridement ultrasound wound healing therapy, or any other wounds

Currently, DBT accounts for over half of the global breast imaging market’s revenue, fuelled by its high average selling price, and popularity in Western Europe, North America and Oceania. These regions are also actively investing in DBT equipment in preparation of breast cancer screening programmes by transitioning to DBT, as seen in the United States.

This is likely to occur in the mid-term as the TOSYMA and TMIST DBT trial results are expected to be released in 2025 and provide strong evidence for its implementation.

As a result, growth for full-field digital mammography (FFDM ) is mostly limited to developing nations. The pricing of DBT is often prohibitive in these regions, making FFDM the predominant solution for the expansion of breast cancer screening and diagnostic capacities. Growth is further fueled by the replacement of outdated analogue mammography systems with newer digital gantries in regions such as Latin America and Asia Pacific.

The ultrasound market represents a smaller proportion of global breast imaging units but is forecast the fastest annual revenue growth of any breast imaging modality, with an average annual increase of 12.0% over the next five years. This growth is driven by the increase in supplementary screening exams and breast density awareness. The recent change in European guidelines by EUSOBI’s also includes the recommendation for supplementary ultrasound when MR is unavailable, which is driving demand further. ABUS is growing at a much faster rate than conventional ultrasound, in China and U.S. particularly, and with a much higher price point, it contributes heavily to the overall growth of the ultrasound market.